We already have the publication of the last report about the American shipments of the past month of NOVEMBER 2021.

The number of shipments is 220.91 Mlbs (-16.1%), lower than the figure of November last year with 263.18 Mlbs, which was a record figure in the history of the months of November.

Regarding the sales of the month, we have a data of 226.02 Mlbs, being 234.95 Mlbs last year, which means -3.80% of sales in the month of November.

Export shipments have been 155.90 Mlbs (-20.2%). Domestic shipments were 65.00 Mlbs (-4.0%).

Regarding the crop, we have an entry of 2,312.08 Mlbs (-4.22%). However, in the total harvest, adding the carryin, we have 2,873.97 Mlbs (+ 2.07%). With a crop input of around 75/80% of the total, each month that passes you can see how the whole of it will be, and it is still difficult with these data that it will be the 2.8 Blbs that he said the objective estimate, being more realistic an a priori harvest between 2.9/3 Blbs as we can observe for now. With these data, we would have a harvest of 2.97 Blbs (last season they were 3.10 Blbs), which added to the carryin of 0.61 Blbs we would go to a total of 3.58 Blbs, when last season we had a total of around of 3.50 Blbs. In other words, we would have a harvest very similar to the last one.

Regarding what was sold and not shipped, we have a total of 753.06 Mlbs (-25.05%) (this data has improved, although little, compared to the -27.70% of last October). In domestic: 338.89 Mlbs (-13.84%) and exports 414.26 Mlbs (-32.37%).

With this situation, a total of 1,247.93 Mlbs (+ 59.16%) would remain unsold (inventory).

With these data we can see that 1.63 Blbs have been sold in general, -19.97% from last year. In the average of shipments of everything we have carried so far, we have -14.99%, less shipped than last season.

Regarding the destination of shipments, countries such as Japan, Belgium, Holland, Sweden (strong rise) or the United Arab Emirates (strong rise) stand out positively. On the negative side, there are many important countries such as Canada, China (very strong decrease), South Korea, Vietnam, India (strong decrease), Germany, France (strong decrease), Italy (strong decrease), Greece, United Kingdom, Turkey, Saudi Arabia (strong drop) or Morocco (very strong drop). In Spain the situation has been very negative, with 10.93 Mlbs this month compared to 20.39 Mlbs the previous year (-46.38%). In total harvest, 51.61 Mlbs have been exported this year and 73.32 Mlbs last year (-29.61%). In Europe in general, 53.06 Mlbs this month compared to 64.25 Mlbs the previous year (-17.42%). In total harvest, -23% has been exported to Europe than last.

These data leave perhaps bearish feelings. It is true that a harvest entry is beginning to be seen that is beginning to move away a little more from the great past harvest, but not as much as expected according to the objective and it will be close to what has been discussed lately. That is, the data in this sense that the report throws is what was predicted colloquially, a harvest that will be between 2.9/3 Blbs.

Otherwise, negative data in general. It is still not possible to exceed shipments month by month last year and it is normal, the goal is very high and it is also normal that they are negative, if there is a lower harvest input of -4.22%, the logical thing, to remain as the Last year, it is having shipments close to this figure, or at least the average of all of them, but for now the average is -14.99%, much lower. There is still a problem of sales that has been dragging since the beginning of the harvest that is taking a lot to reduce.

The worst part, it may not be the numbers themselves, but the feeling. The month of November, with the decline caused by the previous publication, reaching eventually levels below $ 1.90/lb clearly activating demand and activity until it bounces back and returned to $2/lb and stay there until today in an active way, the feeling was that they had managed to reach numbers similar or higher than those of the previous year, but they have not been able to exceed them, not talking about shipments, that is difficult see it so soon, we talk about sales and activity. As we have said, the goal is very high ...

Therefore, the feeling was better than what can be seen in these data. Even lately we have been able to appreciate an offer reluctant to sell and pressing to cause a rise in prices, with a latent demand, waiting for a final help from this publication. We will see how everything is after this, but it seems that the rise that the offer was looking for will be difficult for now, at least based on these data.

The issue of the lack of water in the valley leaves conflicting opinions depending of the areas where people is located. Is clear that the northern area has higher rainfall and better reserves than the central and southern areas where it has rained much less and a very different situation is seen. In fact, these days it has rained and snowed in the north in numerous ways and this week, if we are seeing rainfall not only in the north, but throughout the valley, we repeat, the situation in the north being nothing to do with that of the rest. . There is still much to see and we will see what happens in general for the 2022 harvest, but for now the opinions are contradictory depending on the area.

On the part of the Spanish almond the situation is exactly the same as in the publication of the last report. As a result of it, the Spanish was in a situation of seeking balance and remained that way until the release of this report, that is, it has not found its place throughout the month.

The supply for its part has not wanted to enter clearly at the prices proposed a priori by the demand, which in turn is very low, around € 4.15/4.25/kg depending on the variety. The demand for its part has not wanted to enter to offer more in such a way that it makes the market stabilize at a more attractive price for the offer and vice versa ...

With which, very very little activity and a lot of apathy on all sides. The season itself is coming to an end, and you have the feeling that it was not particularly lively. With which, the amount that is possibly left for months outside the campaign is quite high, a situation that is already beginning to be seen more frequently.

In Spain, if you can see a very different situation in terms of rains depending on the northern area (more abundant) than the southern area, where they are being very scarce and this is beginning to seriously worry.

The organic for its part continues with a downward trend, reaching levels around €9/kg, even with a lower trend. The activity is very low in recent weeks and this has caused some discontent in the supply, because it has given the feeling that there was a bubble where prices reached very high, the shell was paid very expensive, for now it will deflate ... we will see at which price it stabilizes.

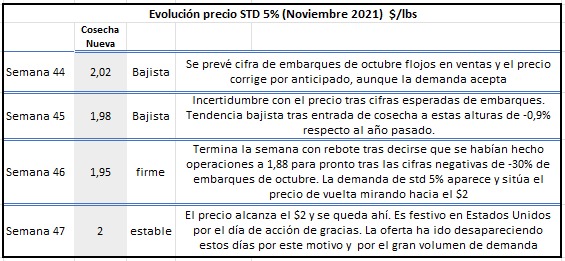

In addition, we offer a table of the evolution of the month of November regarding the American almond that can help to better understand this situation.

We hope this helps.

Thank you very much.