We already have the release of the latest report on American shipments from last FEBRUARY 2022.

The number of shipments is 199.16 Mlbs (-15.0%), lower than the figure for February last year with 234.21 Mlbs.

Regarding sales for the month, we have a figure of 215.03 Mlbs, compared to 188.90 Mlbs last year, which means +13.83% of sales in the month of February.

Export shipments have been 145.78 Mlbs (-11.1%). Domestic were 53.38 Mlbs (-24.0%).

Regarding the harvest, we have an entry of 2,892.03 Mlbs (-6.33%). However, in the total harvest, adding the carryin, we have 3,442.32 Mlbs (-0.96%). Last year, between February and the end of the season, 19.50 Mlbs entered. If we add that figure to this year's entry, we see how the harvest will be around 2.90 Blbs, as has been commented on in previous reports.

Regarding what was sold and not shipped, we have a total of 857.35 Mlbs (-3.33%) (this has improved compared to -9.73% last January). Broken down, it would be, with respect to the domestic, 348.66 Mlbs (-0.32%) and the export 508.70 Mlbs (-5.29%). This figure should be better than last year, despite the fact that the distance is closing. Everything that cannot be shipped because there is no more logistical possibility, goes to this point. Therefore, there should be more than normal, as this problem did not occur last year.

With this situation, a total of 1,146.81 Mlbs (+30.81%) would remain unsold (inventory).

With these data we can see that 2.30 Blbs have been sold in general, -11.68% compared to last year when 2.60 Blbs had been sold. With only -0.96% availability of total almonds, there is actually less sales compared to the same harvest as -10.72% of last year around these dates (hence the high inventory or unsold that we have mentioned), reducing the slab of -25.28% with which the campaign began. The bad first months of the campaign continue to be paid. In the average of shipments of everything that we have carried out so far, we have a -16.01%, less shipped than last season.

Therefore, if for now a total of 1,438.16 Mlbs has been shipped and we see an average of around 200 Mlbs per month of maximum shipping capacity, by the end of the harvest (5 months) 1,000 Mlbs would be shipped. If we add this to the total shipped to date, it would be a total of 2,438.16 Mlbs. If we have a total of 3,442.32 Mlbs of harvest, what would be left over (carryin) for the next harvest would be around 1 Blbs.

Regarding the destination of the shipments, countries such as India, Denmark, Italy (strong rise) or the Netherlands (strong rise) stand out positively. On the negative side, important countries appear such as China, South Korea, Belgium, Germany (strong decrease), France (strong decrease), United Kingdom, Saudi Arabia (strong decrease), Turkey (very strong decrease), United Arab Emirates (strong decrease). very strong) or Morocco (very strong descent). In Spain the situation has been positive, with 20.98 Mlbs this month compared to 18.64 Mlbs the previous year (+12.55%). In total, the harvest has been exported this year 98.89 Mlbs and last year 131.64 Mlbs (-24.88%). In Europe in general, 66.71 Mlbs this month compared to 65.05 Mlbs the previous year (+2.55%). In total, the harvest has been exported -21.78% to Europe compared to the last harvest.

With these data we can see that logistical problems continue at the same level as we have seen in recent reports, which will mean, as we have explained, that the carryin will be very high (possibly around 1 Blbs). This generates a very important problem, not only at a financial level, but also at a physical storage level. This (the logistics problem) is something that cannot be solved with prices, but it does affect them. Whatever crop is coming, you start with this outrageous quantity. This is not to say that part of this is not sold, even though sales in general right now are also being lower than last year as we have seen. That is, part of this surplus will be sold and not shipped and another part will be unsold. We will see at the end the % of both. What is clear is that if the problems persist, the new crop will take much longer than normal to reach destinations far from the Americans.

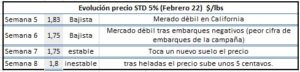

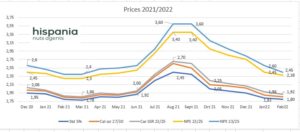

On the other hand, we have seen a very good month of February in terms of sales. It is noted that the first weeks of the month at prices of $1.75/lb for the Std 5% and the rest of the varieties and sizes also very tight, has encouraged the buyer to make a lot of moves. However, after the frost news especially in the northern part of the valley, prices rallied a bit, testing levels of $1.82/1.85/lb on Std 5% for very low activity and its subsequent position around $1.80/1.82/lb today. But these movements took place at the end of February and so far in March, so it has not affected the good sales of February too much.

The real final result of what the frosts may have produced in the coming harvest will be seen in the coming weeks, but the market has been affected by a small rise in prices and a subsequent poor response from the buyer, not only because of this rise, but they also affect other factors such as the Russia/Ukraine conflict that causes not only fear and lack of activity in certain buying countries, but also a change that makes the almond in € higher and with it the greatest loss of interest. It is for all this that the seller has not been able to give the price the push he wanted, especially after everything we are seeing at a general level and the price increase in everything necessary to produce the product.

Today the American seller is presented with a very complicated situation, especially because of what is taking place outside of it and which affects him directly. It is not just about the price, but fundamentally the logistical problem, which entails the conflict and the uncertainty that this generates. We will see how everything external evolves and also the harvest, not only due to frost, but also a lack of water (scarce rains during January and February) that can affect different points of the valley.

On the part of Spanish almonds, the situation continues to be very stable and unchanged. In fact, the situation is the same throughout 2022 so far. Supply is scarce and punctual, as is demand. Because the intensity of both is the same, it causes this stability in the price.

The prices remain the same, €4.05/4.10/kg speaking of communes/valencia propietario/unsized, depending on the delivery and sizes. The rest of monovarietals and sizes continue at the same levels as well.

It is true that everything that has been said about American almonds and their problems is to the benefit of Spanish almonds, in terms of lack of logistical problems, currency exchange fluctuations, delays and with them the foreseeable effect on their quality. The Spanish almond, in terms of price, is getting closer to the American one, which makes it a little more attractive, if possible, for the buyer, who until now has not been in favor of paying the upward differential of the Spanish almond. We will see if with all the advantages that the Spanish has and if the prices are similar, the demand increases, something that is expected but it is true that not much has been seen yet. We insist, it is possible that an unforeseen possibility would open up for the Spanish almond if everything were normal. For now, the buyer does not pay the differential, especially medium / long term, short term if he has no other choice. If the Spanish will be presented with this possibility and knows how to manage it properly, it may have a very good opportunity.

The organic almond continues on its listless path. It is not clear exactly where it stands and has not yet achieved the stability or clarity it needs.

In addition, we offer some tables of the evolution of the month of February regarding the American almond that can help to understand what we have commented.